Understanding Healthcare Costs in the United States

Quick answer: Healthcare costs vary by 2–5× depending on where you receive care, your insurance's negotiated rates, and your deductible status. Typical ranges:

- MRI: $800–$3,000

- CT scan: $500–$2,500

- Colonoscopy: $1,500–$7,000

Healthcare costs vary widely because of three main factors: (1) where care happens (place of service), (2) how insurers price it (negotiated allowed amounts), and (3) your deductible and cost-sharing. This guide explains how those factors work — and how to estimate what you'll actually pay before scheduling care.

The same MRI can cost $800 at an independent imaging center or $3,000 at a hospital outpatient department. The same colonoscopy can cost $1,500 at an ambulatory surgery center or $7,000 at a hospital. The procedure is identical. The setting drives the price difference — and that's something patients can often control.

Most healthcare pricing confusion isn't random — it follows rules most people never learn. Understanding those rules gives you real leverage: knowing how place of service, allowed amounts, and deductible timing work together lets you estimate costs before care, not just understand bills after the fact.

What you'll learn: Why the same procedure can cost 2–5× more depending on setting, how place of service often matters more than the procedure itself, what allowed amounts are and why they determine your cost, and how to use the CostKits framework to estimate your out-of-pocket expenses before scheduling care.

Browse Medical Costs by Category

Select a category below to explore cost guides for specific procedures, including national averages, state-by-state variation, and what drives price differences.

Typical Costs for Common Medical Procedures

Before diving into the framework, here are typical cost ranges for common procedures — from low-cost settings (ambulatory surgery centers and independent imaging) to higher-cost hospital outpatient settings. These ranges reflect allowed amounts under commercial insurance, not billed charges.

| Procedure | Low End (ASC / Independent) | High End (Hospital Outpatient) |

|---|---|---|

| MRI | ~$800 | ~$3,000 |

| CT scan | ~$500 | ~$2,500 |

| Colonoscopy | ~$1,500 | ~$7,000 |

| Knee replacement | ~$15,000 | ~$35,000 |

| Emergency room visit | ~$500 (urgent care) | ~$1,500–$3,500 (ED) |

| Childbirth (vaginal) | ~$5,000 | ~$15,000+ |

Forecast Your Healthcare Costs This Year

Add upcoming visits and your plan details to see how much you're likely to spend — and when you'll hit your deductible or out-of-pocket max. Save your forecast by entering your email.

Why Healthcare Costs Vary (and What Affects Your Medical Bill)

When most people hear "healthcare cost variation," they imagine geographic differences — that care costs more in New York than in rural Alabama. That's true. But the variation within a single city, between facilities just miles apart, is often just as dramatic.

The same procedure can cost very different amounts

A CT scan of the abdomen carries a specific medical billing code — a Current Procedural Terminology (CPT) code that describes what was done. In principle, the same CPT code represents the same service. In practice, what a patient pays for that service can differ by 400 to 600 percent depending on which facility performed it and which insurer is paying.

This happens because the price of a medical service is not set at the procedure level. It is set at the intersection of the provider's billing, the insurer's negotiated discount, and the specific facility where care was delivered. Two hospitals in the same metro area may have negotiated very different rates with the same insurer. A hospital-based CT scan and an independent imaging center CT scan may involve the same equipment, the same quality, and the same radiologist reading — but generate bills that look nothing alike.

Understanding this is the foundation of understanding healthcare costs: there is no single "price" for a medical procedure. There are many prices, determined by where care happens and who is paying.

The hospital is not the only place care happens

Much of American healthcare is delivered outside of hospitals. Physicians see patients in offices and clinics. Imaging scans happen at freestanding imaging centers, not just hospital radiology departments. Surgeries that once required overnight hospitalization now routinely occur in ambulatory surgery centers. Emergency care starts in the ED but may or may not result in a hospital admission.

Each of these settings operates under a different fee structure and, typically, generates a different total cost for the same service. The setting — what the healthcare industry calls the place of service — is one of the most powerful determinants of your bill. In many cases, it matters more than the procedure itself.

Insurance changes what you personally pay

Even after you know the facility and the procedure, your actual out-of-pocket cost depends on your specific health insurance plan and where you are in your benefit year. Insurers negotiate discounted rates with providers — called allowed amounts — and your cost-sharing (deductible, copay, coinsurance) is applied to that negotiated rate, not to whatever the provider originally billed.

If you haven't met your deductible, you may pay a large portion of a claim out of pocket. If you've already exceeded your deductible, you might pay only your coinsurance percentage. If you've reached your out-of-pocket maximum, you pay nothing additional for covered in-network services. The same procedure performed on different dates within your plan year can cost you very different amounts.

Healthcare bills are often multiple claims combined together

One of the most common points of confusion when patients receive medical bills is that a single encounter — a surgery, a delivery, an ER visit — typically generates multiple separate claims from multiple separate providers. Most hospitals and physician groups bill independently, even when they work together to care for you.

A joint replacement, for example, might produce: a facility claim from the hospital, a professional claim from the orthopedic surgeon, a separate claim from the anesthesiologist, and potentially additional claims from the assistant surgeon or hospitalist. Each claim goes through your insurance separately, is applied to your deductible separately, and may come from a different billing organization. This is why patients often say they "kept getting bills" after a procedure they thought they had already paid for. Learn more in our guide to how medical bills work.

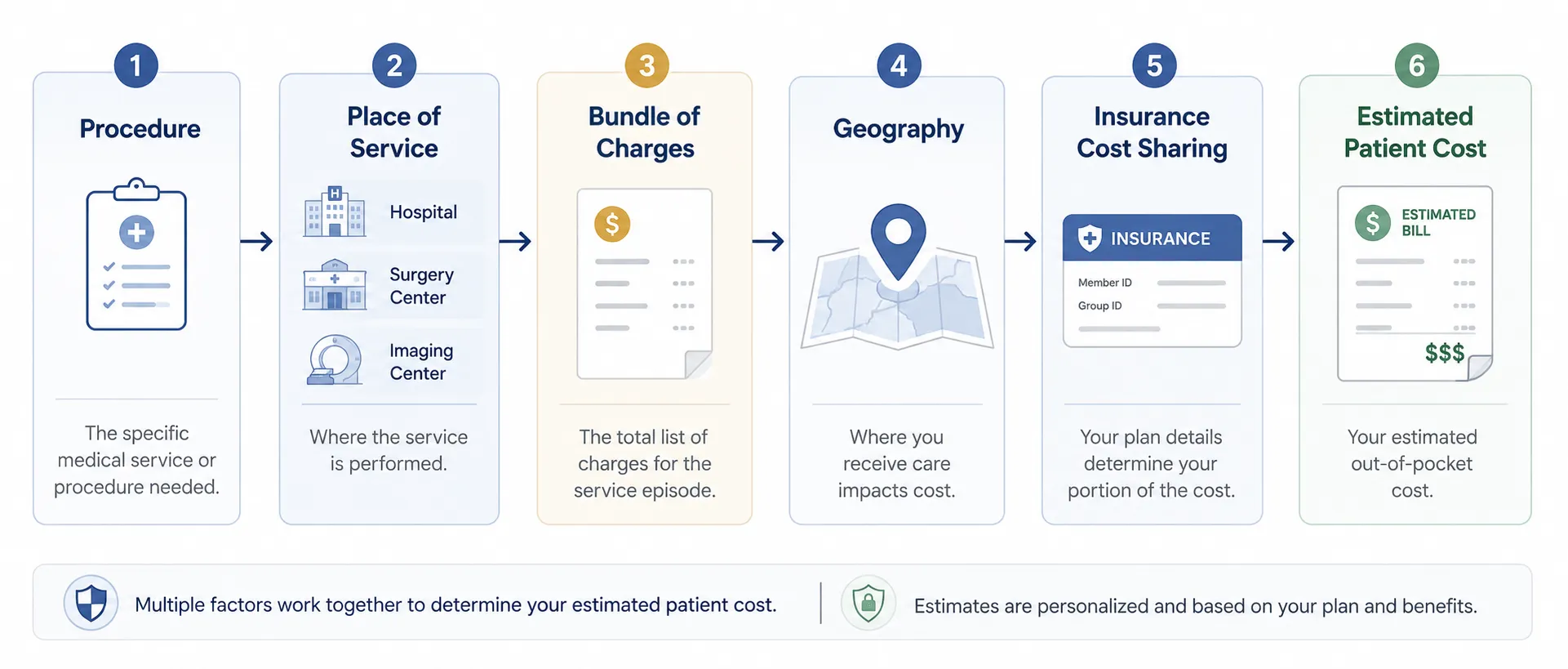

The CostKits Framework for Understanding Medical Costs

Rather than treating healthcare costs as unpredictable, CostKits approaches them as a structured problem with identifiable variables. Working through those variables — in order — makes cost estimation meaningful and actionable.

Core insight: The setting often matters as much as the procedure itself. Changing where a procedure happens can change the cost more than almost any other variable under a patient's control.

Identify the procedure or service

What exactly is being done? Medical services are coded using CPT codes that define the specific procedure. Knowing the specific procedure — not just the general category — determines which billing codes will be used and sets the base for cost estimation.

Identify the place of service

Where will the procedure happen? An office, a freestanding imaging center, a hospital outpatient department, an ambulatory surgery center, or an inpatient hospital stay? This is the most important variable in determining total cost, and often the most overlooked. Explore our procedure cost guides to see how setting affects specific procedures.

Understand the likely bundle of charges

What claims will this encounter generate? Most procedures create at least a facility claim and a professional claim. Surgeries may add anesthesia. Biopsies may add pathology. Understanding the likely bundle — not just the main procedure — gives a more complete picture of total exposure.

Adjust for geography and local market pricing

Healthcare costs vary by region due to local wage levels, hospital market concentration, and insurer bargaining power. A procedure that costs $2,000 in one market may cost $4,500 in another for structural reasons unrelated to quality. Geographic adjustment is built into Medicare payment rates and influences commercial rates as well.

Estimate how insurance changes the final patient responsibility

Apply your plan's cost-sharing rules to the allowed amount for each claim. Are you pre-deductible or post-deductible? What is your coinsurance percentage? Have you reached your out-of-pocket maximum? Each of these factors determines how much of the allowed amount you personally owe. Use our cost forecasting tool to estimate your annual out-of-pocket exposure.

This five-step framework doesn't eliminate uncertainty — healthcare billing has genuine complexity that no single guide can fully resolve. But it identifies where the variation comes from and which questions to ask before receiving care rather than after.

Want to estimate your cost? Try the CostKits cost estimator → Enter your plan's deductible and coinsurance to see what you'd actually owe for common procedures.

Why the Place of Service Often Matters Most

The place of service is the single most actionable cost variable for most patients. For elective procedures, where care happens is often something a patient can influence — if they know to ask. This section explains each major care setting, how its billing structure differs, and what typical procedures look like in each context.

Office and clinic visits

When a physician sees you in their own office or an independent clinic, you typically receive a single professional claim for the evaluation and management (E&M) visit. There is no separate facility fee. Office-based procedures — minor biopsies, joint injections, simple skin removals — are often billed as add-on codes to the office visit, keeping total cost relatively modest.

However, if a physician's office is part of a hospital system and has been designated as a hospital outpatient department, the same visit may generate a facility fee on top of the professional fee — even if you never stepped inside a hospital building. This is one of the more surprising cost distinctions patients encounter.

Common procedures: Office visits, minor procedures, vaccinations, basic labs drawn in office.

Independent imaging centers

Freestanding imaging centers — not affiliated with hospitals — typically offer the same quality imaging equipment and the same radiologists as hospital systems, but at materially lower rates. This is because they do not carry the overhead structure of a hospital and are not subject to the same facility fee billing rules.

At an independent imaging center, a patient typically receives one combined claim (or sometimes a facility and professional claim that are both priced at outpatient center rates, not hospital rates). For MRIs, CT scans, and X-rays, the difference between an independent center and a hospital-based imaging department can be substantial.

Common procedures: MRI scans, CT scans, X-rays, ultrasounds.

Hospital outpatient departments (HODs)

When a procedure is performed at a hospital-based outpatient department — even if you walk out the same day — the billing structure is fundamentally different from a non-hospital setting. Hospital outpatient departments bill under a facility fee structure that is separate from the physician's professional fee. Both claims go through your insurance, and both count toward your deductible and out-of-pocket maximum — but the facility component alone can be several times what an independent center charges for the same service.

Hospital outpatient departments carry higher overhead: emergency standby capacity, accreditation requirements, broader support staff. Those costs are embedded in the rates they negotiate with insurers, and those rates are passed through to patients via cost-sharing.

Common procedures: Colonoscopies, endoscopies, complex imaging, infusions, outpatient surgeries.

Ambulatory surgery centers (ASCs)

Ambulatory surgery centers are dedicated outpatient surgical facilities designed specifically for procedures that do not require an overnight hospital stay. They offer a middle ground: more capability than an office but lower overhead than a hospital outpatient department. Medicare pays ASCs significantly less than hospital outpatient departments for many of the same procedures, and commercial insurers often follow a similar differential.

For patients, this typically translates to meaningful savings on elective surgeries when an ASC is an appropriate care setting. Procedures like colonoscopies, upper endoscopies, cataract surgeries, and knee arthroscopies are routinely performed at ASCs with the same clinical outcomes as hospital-based settings.

Common procedures: Colonoscopies, cataract surgery, knee procedures, hernia repairs, outpatient orthopedics.

| Procedure | Ambulatory Surgery Center | Hospital Outpatient Dept. |

|---|---|---|

| Colonoscopy | ~$1,500–$3,000 | ~$3,000–$7,000 |

| Upper endoscopy (EGD) | ~$1,200–$2,500 | ~$2,500–$5,500 |

| Knee arthroscopy | ~$5,000–$9,000 | ~$9,000–$18,000 |

Emergency departments

Emergency department visits generate a facility fee structured around acuity levels (typically Level 1 through Level 5, from minor to critical). Even a Level 2 or Level 3 ED visit — for a minor injury or illness that could, in hindsight, have been treated at urgent care — carries a facility charge that is substantially higher than a comparable non-hospital visit. In addition to the facility charge, you receive a separate claim from the emergency medicine physician group, which typically bills independently from the hospital.

Emergency care is, by definition, not always planned — and avoiding the emergency department for genuine emergencies is not a financial recommendation. But for situations where urgency is uncertain (a non-life-threatening injury, a fever in a child overnight), understanding that urgent care centers carry dramatically lower facility costs than EDs is worth knowing.

Common procedures: Trauma, acute illness, diagnostic workups under emergency conditions.

Inpatient hospital stays

When a patient is formally admitted to a hospital — rather than treated and discharged the same day — the billing transitions to an inpatient structure. Medicare reimburses inpatient stays using a DRG (Diagnosis-Related Group) system, which assigns a fixed payment based on the admission diagnosis and complications rather than itemizing every service provided. Commercial insurers may use case rates, per diems, or their own DRG-based methodologies.

From a patient perspective, inpatient stays typically involve the highest dollar amounts and the greatest billing complexity. Multiple physicians from different specialties may see the patient on different days, each billing independently. Procedures, labs, imaging, and medications all generate their own line items in the facility bill. Childbirth and major surgical procedures are common reasons for planned inpatient admissions.

Common procedures: Childbirth, major surgery, serious illness requiring monitoring overnight or longer.

Understanding the Difference Between Billed Charges, Allowed Amounts, and What You Owe

The gap between what a hospital bills and what a patient actually owes is one of the most confusing aspects of American healthcare. Understanding three distinct concepts — billed charges, allowed amounts, and patient cost-sharing — clarifies this considerably.

Billed charges are often not the real price

When a hospital or physician submits a claim to your insurance, the original amount billed is called the billed charge or chargemaster rate. These are the "list prices" of healthcare services, set by each provider. They are rarely what anyone actually pays.

In most commercial insurance transactions, the billed charge is the starting point of a negotiation that already happened — when your insurer signed a contract with the provider. That contract specifies the allowed amount: the actual payment the insurer will make for each service. The billed charge is typically much higher than the allowed amount. The difference is written off by the provider as a contractual adjustment.

Allowed amounts are usually more important

The allowed amount — sometimes called the allowable charge, negotiated rate, or contracted rate — is the maximum amount your insurance plan will pay for a covered service from an in-network provider. Your cost-sharing (what you owe personally) is calculated as a percentage of the allowed amount, not the billed charge.

If a provider bills $6,000 for an outpatient procedure but the allowed amount under your plan is $2,400, the $3,600 difference is written off. Your deductible and coinsurance are then applied to the $2,400. Understanding this distinction is fundamental to reading an Explanation of Benefits (EOB) from your insurer.

Important: Allowed amounts vary by plan and by provider. The same procedure at the same facility may have a different allowed amount depending on which insurance plan you have. This is why asking your insurer "what is the estimated allowed amount for this procedure at this facility?" is more useful than asking what the procedure "costs."

Deductibles, copays, and coinsurance

Once the allowed amount is established, your plan applies its cost-sharing rules to determine your patient responsibility:

- Deductible: The annual amount you must pay out-of-pocket before your insurance begins sharing costs for most services. Until you meet this threshold, you typically pay 100% of the allowed amount for non-preventive services.

- Copay: A fixed dollar amount you owe per visit or prescription, often not tied to the allowed amount. Common for primary care and specialist office visits.

- Coinsurance: A percentage of the allowed amount you owe after meeting your deductible. A 20% coinsurance means you pay 20% of the allowed amount; your plan pays 80%.

- Out-of-pocket maximum: The annual ceiling on your total cost-sharing. Once reached, your plan covers 100% of covered in-network costs for the remainder of the plan year.

These elements combine to produce your actual patient responsibility for each claim — and the combination looks different depending on where you are in the plan year.

Preventive vs. diagnostic care

Under the Affordable Care Act, certain preventive services — including routine screenings like colonoscopies for average-risk patients at appropriate ages — must be covered at no cost to the patient when delivered by in-network providers. This is an important distinction from diagnostic care.

A colonoscopy ordered as a routine preventive screening is typically covered at 100% with no deductible or coinsurance applied. However, if the physician removes a polyp or discovers a condition requiring intervention during that same procedure, the claim may be reclassified as diagnostic or surgical — subject to normal cost-sharing rules. This is a common and legitimate source of unexpected bills, and it is worth asking your physician and insurer in advance how a procedure will be coded based on what they expect to find.

Why timing within the year matters

Because deductibles reset annually, the timing of elective procedures within your plan year can meaningfully affect your cost. Scheduling a significant procedure early in the year means you will likely pay a larger share out of pocket before your deductible is met. Scheduling after meeting your deductible — if you have substantial prior-year spending — shifts the cost to coinsurance only.

This dynamic particularly matters for households with ongoing healthcare needs: managing the sequencing of planned procedures relative to deductible thresholds is one of the few direct levers patients have over their annual healthcare spending.

Example Medical Cost Scenarios

Abstract explanations of healthcare cost structure are easier to absorb with concrete examples. The scenarios below illustrate how the framework applies in practice. All cost figures are illustrative only and do not represent actual negotiated rates for any specific plan, facility, or geography.

Example: Colonoscopy at an ASC vs. a hospital outpatient department

Two patients, same insurer, same plan, same $1,500 deductible, same 20% coinsurance. Both have a routine screening colonoscopy. Both are pre-deductible at the time of the procedure.

Patient A has the procedure at a freestanding ambulatory surgery center. The total allowed amount for facility plus anesthesia is approximately $2,200 (illustrative). She pays her $1,500 deductible and then 20% coinsurance on the remaining $700 — a total of roughly $1,640.

Patient B has the same procedure at a hospital outpatient department. The total allowed amount for facility plus anesthesia is approximately $5,800 (illustrative). He pays his $1,500 deductible and then 20% coinsurance on the remaining $4,300 — a total of roughly $2,360.

The procedure is identical. The physician may be the same. The setting produces a difference of over $700 in patient responsibility for a single encounter.

These are illustrative examples only. Your plan's allowed amounts, deductible, and coinsurance will differ. See our colonoscopy cost guide for more detail.

Example: MRI at an imaging center vs. a hospital system

A patient needs an MRI of the knee for persistent pain. Her physician refers her to the imaging department at the affiliated hospital system. The allowed amount for a hospital outpatient MRI, covering both facility and professional read, is approximately $2,800 (illustrative).

Before scheduling, she asks her insurer if there are in-network freestanding imaging centers. There are two nearby. The allowed amount at an independent center for the same MRI — same equipment, same quality, same radiologist credential — is approximately $850 (illustrative).

She has not yet met her deductible. At the hospital, she would owe approximately $2,800 out of pocket until her deductible is satisfied. At the imaging center, she would owe approximately $850. The difference is entirely attributable to setting, not clinical quality.

These are illustrative examples only. See our MRI cost guide for national cost comparisons.

Example: Childbirth with and without complications

Childbirth is typically the highest healthcare expenditure many families experience in a single year. A vaginal delivery with a 2-night stay generates claims from the hospital (facility), the delivering OB physician, and the anesthesiologist (for an epidural). If the newborn requires any specialized care, neonatology billing adds additional claims.

A planned vaginal delivery at a hospital with a $4,000 out-of-pocket maximum might result in the patient reaching that maximum — paying $4,000 for what is a $15,000–$25,000+ total allowed-amount event (illustrative). A cesarean delivery, with a longer stay and more complex facility billing, typically generates higher allowed amounts and may still hit the same out-of-pocket maximum — but can leave a larger balance if the patient hasn't hit it.

Families expecting a birth in a given plan year often benefit from timing their plan enrollment to cover the delivery at the start of a new plan year rather than mid-year, maximizing the time their deductible is met before delivery occurs.

Illustrative examples only. See our childbirth cost guide for national and state-level data.

Example: Emergency department visit that becomes an inpatient stay

A patient arrives at the emergency department with chest pain. After evaluation — including an EKG, blood work, and imaging — the hospital determines the patient needs to be admitted for monitoring. What began as an outpatient ED visit transitions to an inpatient admission.

The billing split changes at this point. The ED facility charge is separate from the inpatient facility charge. The emergency physician's bill is separate from the hospitalist or cardiologist bills during admission. Labs, imaging, and any procedures generate their own claims. A 2-night admission for a cardiac event might generate 5 to 8 separate bills from different providers over the following 4–8 weeks.

Patients in this situation often benefit from requesting an itemized bill from the hospital and reviewing each claim with their insurer's EOBs to verify that all claims were processed at in-network rates and at the correct benefit level.

Illustrative example only. See our emergency room cost guide for more.

How People Track Healthcare Costs Today

Most American families have no systematic way to track their healthcare costs. They receive bills from multiple providers, explanation of benefit (EOB) letters from their insurer, and occasional statements from their HSA or FSA administrator — each in a different format, arriving on a different schedule, and organized around provider and plan logic rather than patient logic.

Spreadsheets and paper bills

Many organized families track healthcare spending in a spreadsheet, manually entering each bill as it arrives. This works reasonably well for retrospective tracking but requires discipline to maintain and offers no forecasting capability. A single surgery can generate enough separate bills and EOBs to make reconciliation genuinely confusing even for attentive patients.

Insurance portals and EOBs

Most large insurers offer online portals where members can view their Explanation of Benefits documents, track deductible accumulation, and see claims history. These portals are useful for claims data but are organized around the insurer's administrative needs rather than the patient's financial planning needs. Finding your year-to-date deductible progress, for example, is often straightforward. Projecting what a scheduled procedure will cost, given your current deductible position, requires manual calculation.

HSA and FSA tracking

Patients with Health Savings Accounts (HSAs) or Flexible Spending Accounts (FSAs) have an additional tracking layer: eligible expenses must be documented against their account activity, and the funds must be managed relative to annual contribution limits. HSA administrators provide statements, but correlating HSA distributions with specific medical claims typically requires manual effort.

Why it is difficult to estimate future costs

Healthcare cost estimation is genuinely difficult for several interconnected reasons. You may not know the exact CPT code for a planned procedure. You may not know what the allowed amount for that procedure at that facility will be under your plan. You may not know whether additional claims (anesthesia, pathology, assistant surgeon) will be generated. And your deductible position at the time of care depends on claims that haven't yet occurred.

These challenges do not mean estimation is impossible — they mean it requires a structured approach that most available tools don't provide.

How CostKits Helps

CostKits was built around the insight that healthcare cost confusion is primarily a structural problem, not an information problem. The information exists — in claims data, in plan documents, in Medicare rate schedules. What has been missing is a way for individuals to use that information to make sense of their own situation.

Save and organize healthcare expenses

CostKits gives you a single place to save healthcare expenses as they occur. Rather than managing paper bills from five different providers and EOBs from your insurer, you can log each expense — or import it — and have your spending organized by date, provider, family member, and type of service.

Track deductible and out-of-pocket spending

Knowing exactly where you stand against your deductible at any point in the year is one of the most practically useful pieces of financial information a healthcare consumer can have. CostKits tracks your accumulated deductible and out-of-pocket spending so you always know your current cost-sharing position — and can factor that into decisions about timing elective care.

Understand how procedure setting affects cost

For procedures where setting is a choice, CostKits provides illustrative cost comparisons across care settings — office, imaging center, hospital outpatient department, ASC — for common procedures. This doesn't tell you what your insurer will specifically pay, but it provides the structural information needed to ask the right questions when scheduling care.

Forecast future healthcare expenses

Using your plan structure — deductible, coinsurance, out-of-pocket maximum — and your spending history, CostKits can help you project what your remaining annual exposure is likely to be. This is particularly useful for families managing ongoing care, planning an elective procedure, or preparing for a known high-cost event like a delivery. Try our cost forecasting tool.

Compare common procedures and cost ranges

CostKits maintains cost guides for common medical procedures across all 50 states, covering the range of costs under Medicare, commercial insurance, and cash pay scenarios. These guides exist to give patients context — a starting point for understanding what a procedure typically costs before they receive a bill they've never had a reason to anticipate. See our data & pricing methodology for exactly where these numbers come from and how facility data is matched.

Your Healthcare Budget

You can create a free CostKits account with your email to save healthcare expenses, track your deductible progress, and organize your family's bills in one place. Optional subscription features provide additional forecasting, budgeting, and cost-planning tools — so you can plan for healthcare costs the way you plan for any other major expense.

Create a Free Account