Pull your EOBs, sum the applied-to-deductible column, and subtract from your deductible. An actuary's step-by-step method for knowing where you stand — and what to do about it.

The first step in taking control of your healthcare spending is tracking costs using a simple tracker like below, where you can add past or future visits and your insurance information. You can use this for free and can save the forecast by entering your email.

Save your estimate so you know exactly what you'll pay next time →

The question surfaces every fall: have I spent enough this year to hit my deductible — and does the answer change what I should schedule before December? The good news is that this is a calculation, not a guess. Your Explanation of Benefits (EOB) contains the number you need, and once you have it, the next step is clear.

Will I Hit My Deductible This Year? How to Tell

Short answer: Pull every EOB issued since your plan year started and sum the "applied to deductible" column. Subtract that total from your deductible amount. If the remaining balance is smaller than your expected care for the rest of the year, you will likely hit your deductible — and any care above that point will cost only your coinsurance share. If the balance is larger, you probably won't, and that changes whether rushing to schedule elective care makes financial sense.

Contents

- What a deductible actually is

- When this question matters most

- How to check your deductible progress

- A worked example

- What to do once you know your answer

- Frequently asked questions

What a deductible actually is

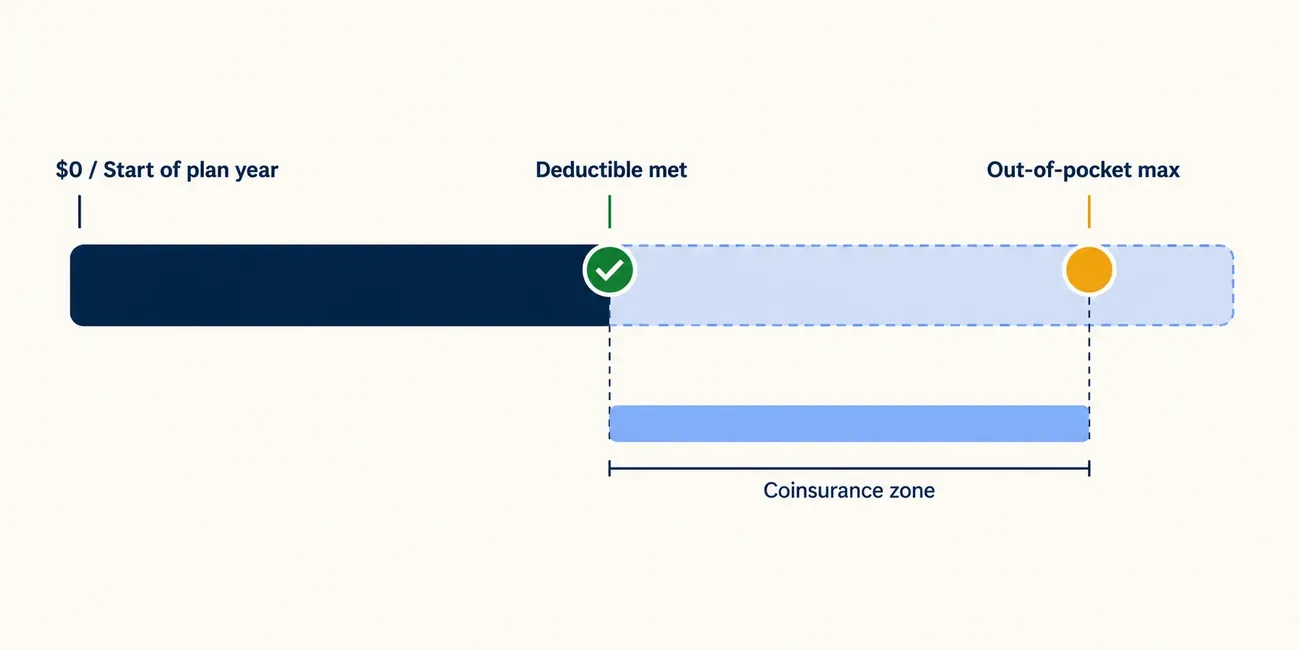

A deductible is the dollar amount you pay toward covered, in-network care before your health plan begins sharing costs. It resets at the start of each plan year — not whenever you want it to, but on your plan's anniversary date (usually January 1 for most Marketplace and many employer plans, though employer plans can reset on any date).

Met your deductible or nowhere close? The answer changes what the same care costs you this year.

The free Deductible Strategy Workbook gives you:

- ✓ A where-am-I calculator that pins down exactly where you stand on your deductible

- ✓ A now-vs-wait decision worksheet for timing care before or after your plan resets

- ✓ Worked examples showing how timing the same procedure changes what you owe

- ✓ A year-end planning checklist to run before your deductible starts over

- ✓ Print-and-fill — sit down with your EOBs once and know your number

Free — we'll email it to you now.

We'll email it to you immediately. No account required, no spam.

The mechanics work like this: before you've met the deductible, you pay 100% of the allowed amount for most covered services. Once you cross it, your plan activates cost-sharing — typically coinsurance (a percentage, like 20%) or copays. A third threshold, your out-of-pocket maximum, caps your total annual exposure: once you hit it, the plan pays 100% of covered, in-network costs for the rest of the year, and your share drops to zero.

Two versions of the deductible matter depending on your coverage:

- Individual deductible: only your own spending counts toward it.

- Family deductible: if you have family coverage, some plans also have a combined family threshold — spending by any covered family member can satisfy it, even before individual limits are reached.

One important carve-out: most preventive care (annual physicals, recommended screenings, specific immunizations) must be covered at no cost on ACA-compliant plans. It doesn't go through your deductible. Knowing this matters because a "preventive" visit that turns diagnostic — say, a colonoscopy that removes a polyp — can shift mid-procedure from cost-free to deductible-subject.

When this question matters most

Knowing your deductible progress has a clear payoff when any of these apply:

You have elective care on your list. A planned imaging study, outpatient procedure, or specialist visit has a very different cost depending on whether you've met your deductible before you schedule it. Timing it before vs. after the plan year reset can mean paying your coinsurance share vs. the full allowed amount all over again.

It's Q3 or Q4. Most of your plan year is behind you, so your deductible history is long enough to make a meaningful projection. Earlier in the year, you have less spending data and more time for circumstances to change.

Your FSA has a year-end balance. Flexible spending account funds generally expire at year-end or a short grace period after it — unused money is forfeited. If you're close to your deductible, scheduling remaining care burns through those funds before they disappear.

You're deciding whether to switch plans at open enrollment. If you switch to a new plan in January, your deductible resets to zero under the new plan, regardless of what you spent on the old one. Understanding your current progress helps you model whether finishing the year on your old plan (to capture accumulated deductible progress) vs. switching to a lower-premium plan is the better move.

How to check your deductible progress

The authoritative source is your Explanation of Benefits (EOB), not your insurer's online deductible tracker. Member portals can lag by two to four weeks and sometimes miss certain claim types. EOBs process each claim individually and show exactly what applied to the deductible, line by line.

Step 1: Find your deductible amount. Get your plan's Summary of Benefits and Coverage (SBC) — your insurer or HR department can provide it. Locate your individual deductible (and family deductible, if applicable). Note your plan-year start date: this tells you which EOBs to pull.

Step 2: Collect all EOBs for the current plan year. Log into your insurer's member portal and download every EOB issued since your plan-year start date. Most insurers allow PDF downloads. If you received care from multiple providers, you'll have multiple EOBs — collect them all.

Step 3: Sum the "applied to deductible" column. On each EOB, find the column or line labeled "applied to deductible," "amount applied," or similar. Add these amounts across every EOB. This running total is your cumulative deductible spending for the year.

Step 4: Calculate your remaining balance. Subtract your cumulative total from your deductible:

Remaining = your deductible − cumulative "applied to deductible"

A result of zero or less means your deductible is met. A positive number is what you still owe before cost-sharing activates.

Step 5: Estimate expected remaining care. List any care you expect before your plan year ends — scheduled procedures, specialist follow-ups, ongoing therapy, prescription refills, or any recommended care you've been putting off. Get rough cost estimates for each. Providers are required to give you a written good-faith estimate before non-emergency scheduled care under the No Surprises Act (effective January 2022).

Step 6: Compare and decide. If your expected remaining care costs more than your remaining deductible, you'll likely hit it — and care above the threshold will cost only your coinsurance share. If expected remaining care costs less, you probably won't meet it this year, and the financial argument for rushing elective care before year-end weakens considerably.

A worked example

Illustrative — the numbers below are hypothetical to show the method, not real prices or national averages.

Alex's employer plan runs January–December, with a $2,000 individual deductible and 20% coinsurance after that. His out-of-pocket maximum is $5,000. In September, he pulls his EOBs for the year:

| Date | Service | Applied to deductible |

|---|---|---|

| February 14 | Urgent care visit | $175 |

| April 3 | Lab work | $120 |

| June 18 | Physical therapy (3 sessions) | $420 |

| August 22 | Knee MRI | $650 |

| Cumulative total | $1,365 |

Remaining to deductible: $2,000 − $1,365 = $635

Alex's doctor has recommended a follow-up orthopedic consultation and a cortisone injection. He requests good-faith estimates from billing:

- Orthopedic consult: ~$320 allowed

- Cortisone injection (technical + physician): ~$480 allowed

- Total expected: ~$800

Since $800 > $635 remaining, Alex will likely hit his deductible this year. His estimated patient responsibility: $635 (remaining deductible) + $33 (20% coinsurance on the ~$165 above the deductible) ≈ $668 for both services combined.

If Alex defers both to January, his deductible resets to $2,000, and he'd pay the full ~$800 allowed amount before cost-sharing begins — approximately $130 more. Scheduling before year-end is the financially better move in this scenario.

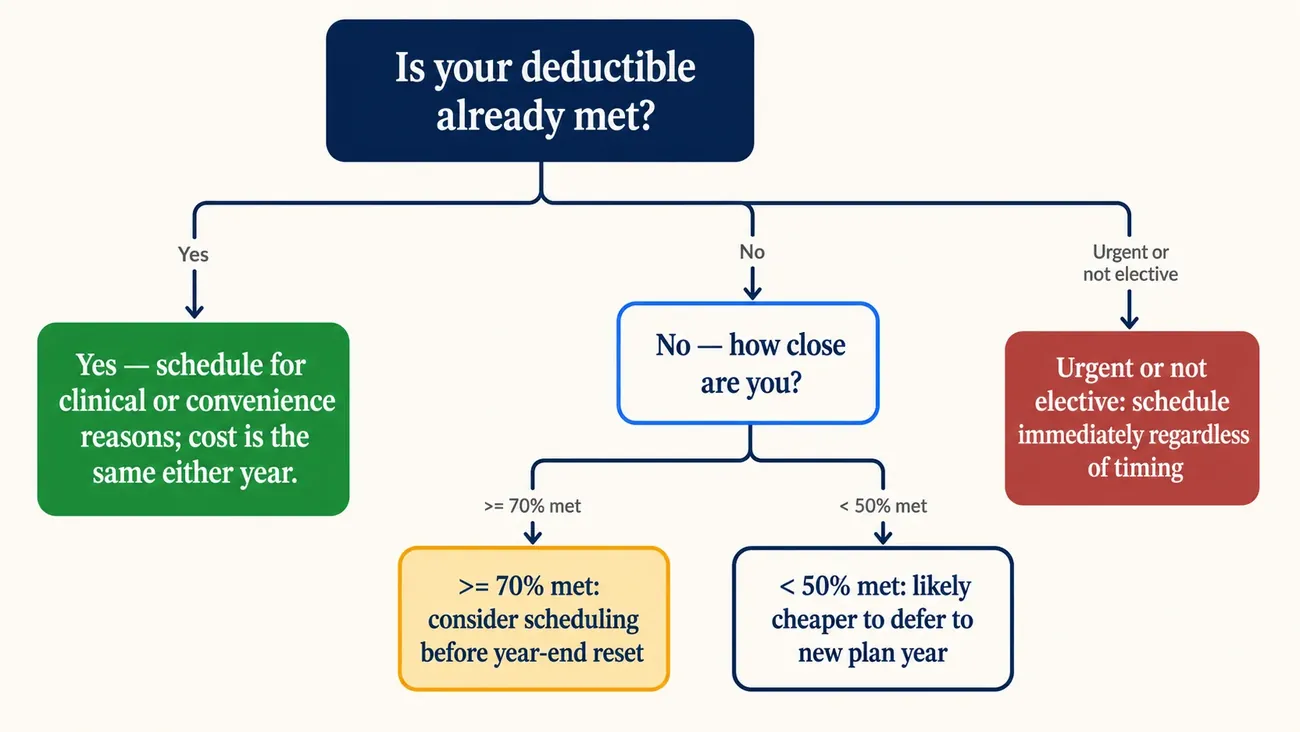

What to do once you know your answer

If you will likely hit your deductible: prioritize scheduling the elective care before your plan year ends. Confirm all providers are in-network, request good-faith estimates, and check whether your FSA balance needs to be used. The Deductible Strategy Workbook walks you through this decision step by step.

If you probably won't hit your deductible: there's less urgency to schedule before the reset. Consider whether the care can wait, or whether coordinating it with other expected spending early in the new plan year makes sense. Early in a plan year, all your spending counts toward a fresh deductible either way.

If you're right on the line: run the numbers for your specific procedure. The break-even point is the remaining deductible amount — if the procedure's allowed cost is close to or exceeds that, scheduling now likely wins.

Get the free Deductible Strategy Workbook — a fillable PDF with the deductible calculator, year-end planning checklist, and the now-vs-wait decision worksheet. Download it below.

Frequently asked questions

How do I know how much I've paid toward my deductible? The most reliable source is the "applied to deductible" column on your Explanations of Benefits — not your provider bills, and not always your insurer's online portal, which can lag by weeks. Sum this column across all EOBs issued since your plan year started.

What counts toward my deductible? Most covered, in-network care counts — office visits, lab work, imaging, procedures, and hospitalizations. What typically does not count: premiums, out-of-network services (on most plans), and services your plan covers before the deductible like preventive care on ACA-compliant plans. Check your SBC for your plan's specific rules.

Does my plan year reset on January 1? Most individual and Marketplace plans do. Employer-sponsored plans can reset on any anniversary date — your SBC or HR department will have the exact date. A non-January reset changes when your deductible strategy calculations apply.

What's the difference between my deductible and my out-of-pocket maximum? Your deductible is the first threshold — once met, insurance begins sharing costs. Your out-of-pocket maximum is the ceiling — once met, insurance pays 100% for covered, in-network care for the rest of the year. Everything you pay toward your deductible counts toward your OOP max, but your OOP max also includes coinsurance and copays you pay after the deductible is met.

What happens the moment I hit my deductible? Your cost-sharing changes immediately. Instead of paying the full allowed amount, you pay only your coinsurance percentage (typically 10–30%) or a copay for each service. This continues until you hit your out-of-pocket maximum, at which point your share drops to $0 for the rest of the year.

Can I see my deductible progress online without pulling EOBs? Most insurers offer a member portal with a running deductible tracker. It's useful for a quick check, but it can lag by two to four weeks and may omit certain claim types. Before making a scheduling decision that depends on an exact number, verify against your actual EOBs.

Does my deductible reset if I change jobs mid-year? Your deductible progress is specific to your plan. If you switch to a new employer's plan, your deductible resets to zero on the new plan — your spending history under the old plan doesn't transfer. Timing a job change around a plan year can meaningfully affect total annual out-of-pocket costs.

How does the family deductible work alongside the individual deductible? It depends on your plan type. Plans with an embedded deductible satisfy each member's individual deductible separately — no single person has to meet the full family limit to get cost-sharing. Plans with an aggregate deductible pool all family spending — you don't get individual cost-sharing until the combined family total meets the family limit. Your SBC will specify which type you have.

Do preventive care visits count toward my deductible? Generally no — ACA-compliant plans are required to cover recommended preventive care at no cost, meaning it bypasses the deductible. However, if a preventive visit leads to a diagnostic service (a biopsy during a screening colonoscopy, for example), the diagnostic portion may be subject to the deductible. This is one of the most common unexpected costs.

What is an HDHP and does it change any of this? A high-deductible health plan has a deductible above a minimum set annually by the IRS — for 2026, that threshold is $1,650 for self-only coverage and $3,300 for family coverage [STAT — VERIFY: IRS Rev. Proc. for 2026 HSA-qualified HDHP thresholds]. The mechanics of how your deductible works are identical to other plans. What's different: HDHP enrollees can contribute to a health savings account (HSA), whose funds roll over indefinitely year to year.

If I'm near my deductible, does it always make sense to schedule care now? Usually, but not always. If the care is truly elective and you're comfortable deferring it, the right answer depends on how much remains, the cost of the procedure, and whether other expected care will push you past the deductible anyway. Run the numbers using the step-by-step method above or the Deductible Strategy Workbook.

What costs count toward my out-of-pocket maximum? Your deductible payments plus coinsurance and copays you pay for covered, in-network care all count toward your OOP max on ACA-compliant plans. Premiums do not count. For 2026 Marketplace plans, the federal ceiling on OOP maximums is $9,200 for self-only coverage and $18,400 for family coverage [STAT — VERIFY: CMS Notice of Benefit and Payment Parameters for 2026]. Employer-sponsored plans can set lower limits but not higher ones.

How do I find my plan's deductible if I lost my Summary of Benefits and Coverage? Call the member services number on your insurance card and ask for your deductible, out-of-pocket maximum, and plan-year reset date. You can also log into your insurer's member portal — most insurers display plan details there. For employer plans, your HR department can pull the current plan documents.

Keep your deductible progress current with CostKits

The six-step method above works well done manually once. Keeping it current as bills and EOBs arrive through the year is what the CostKits tools do automatically:

- Forecast — enter your plan details and expected care to get a projected annual cost and a running view of when you're likely to hit your deductible.

- Analyze — upload a bill or EOB; the tool checks whether the deductible was applied correctly and flags anything that looks off.

- Track — your deductible and out-of-pocket max fill in automatically as care happens, so the question "have I hit my deductible yet?" has a live answer at any time.

Related articles

- Procedure Timing and Deductibles: When to Schedule Care

- How to Estimate Your Out-of-Pocket Costs Before Care

- How to Read an EOB (Explanation of Benefits)

- Deductible vs. Out-of-Pocket Max: What Families Need to Know

- Colonoscopy costs by state

Related Cost Information

About the author

John Caruso, FSA, MAAA is a healthcare actuary with over 20 years of experience in insurance pricing, medical billing systems, and healthcare cost analytics. As founder of CostKits, he built the platform to give families the same cost-transparency tools that insurers and providers use internally. He writes from the actuarial side of the table — the same perspective that sets the rules he's explaining.

Met your deductible or nowhere close? The answer changes what the same care costs you this year.

The free Deductible Strategy Workbook gives you:

- ✓ A where-am-I calculator that pins down exactly where you stand on your deductible

- ✓ A now-vs-wait decision worksheet for timing care before or after your plan resets

- ✓ Worked examples showing how timing the same procedure changes what you owe

- ✓ A year-end planning checklist to run before your deductible starts over

- ✓ Print-and-fill — sit down with your EOBs once and know your number

Free — we'll email it to you now.

We'll email it to you immediately. No account required, no spam.

Related Articles

Interested in understanding healthcare costs and managing your medical expenses?

- Deductible vs Out-of-Pocket MaximumLearn how insurance cost-sharing works and what you actually pay

- Cost ExplorerBrowse procedures and compare prices across the country

- CT Scan Cost GuideFind detailed CT scan pricing for your state

- MRI Cost GuideCompare MRI pricing and understand imaging costs

- X-Ray Cost GuideCompare X-ray pricing across states—one of the most affordable imaging procedures

- Colonoscopy Cost GuideUnderstand colonoscopy pricing and your out-of-pocket costs by insurance type

- New GuidesExplore our latest healthcare guides on costs, insurance, and medical billing

About the Author

John Caruso, FSA, MAAA

Healthcare actuary with 20+ years of experience in insurance pricing, medical billing systems, and healthcare cost analytics. Founder of CostKits.

Connect on LinkedIn →Ready to take control of your healthcare costs?