A step-by-step framework for forecasting your family's healthcare costs for the year — turn last year's spending, your known events, and your deductible into a monthly set-aside you can actually plan around.

The first step in taking control of your healthcare spending is tracking costs using a simple tracker like below, where you can add past or future visits and your insurance information. You can use this for free and can save the forecast by entering your email.

Save your estimate so you know exactly what you'll pay next time →

Compare Healthcare Costs Near You

See what hospitals and clinics near you charge for common procedures — before you schedule your visit.

| # | Provider | City | Distance | Cost Signal |

|---|

Cost signals are based on CMS hospital price transparency data and Medicare fee schedules. Actual costs depend on your insurance plan, deductible status, and network tier. Get your personalized estimate →

You can forecast your healthcare costs for the year with reasonable accuracy — not by predicting which emergencies will happen, but by adding up what's predictable and sizing a buffer for what isn't. Most families treat healthcare as a string of surprises, yet the largest pieces (premiums and routine care) barely move, and the scary part has a ceiling built into your plan: your out-of-pocket maximum.

Forecasting your healthcare costs is easier with a worksheet in hand.

The free Annual Healthcare Budget Planner gives you:

- ✓ A one-page annual budget worksheet that produces your monthly set-aside

- ✓ A major-event checklist so a surgery or new baby never blindsides your plan

- ✓ A deductible worksheet that anchors your buffer to your out-of-pocket max

- ✓ Worked forecast examples you can model your own year on

- ✓ Print-and-fill — bring it to open enrollment or the start of your plan year

Free — we'll email it to you now.

We'll email it to you immediately. No account required, no spam.

This guide walks through a simple, repeatable framework for turning last year's spending, the events you already know are coming, and two numbers from your insurance plan into an annual budget — and a monthly amount to set aside. It's the same logic a forecast tool automates, done here by hand so you understand every step.

How to Forecast Your Healthcare Costs for the Year

Key takeaways

- Healthcare costs are more predictable than most families think — they follow a pattern that repeats year to year.

- Last year's spending creates your baseline (your floor).

- Your out-of-pocket maximum creates your ceiling — the most you can owe for covered, in-network care.

- Known procedures and events fill in the middle.

- The result becomes your monthly healthcare set-aside — money decided in advance, not borrowed from a future month.

- A good forecast isn't a single number; it's a planned range with a monthly funding amount attached.

The short answer

To forecast your healthcare costs for the year: start with what you actually paid last year, add the cost of any major events you already know are coming, then size a surprise buffer against your plan's out-of-pocket maximum — the most you can owe for covered, in-network care in a year. Add those together for an annual budget, and divide by 12 to get a monthly set-aside. You won't predict the exact bill, but you'll know the range and have the money waiting.

Why this works: healthcare spending isn't random — it's bounded. Premiums are fixed. Routine care follows last year's pattern. And your plan caps your worst case. Once you see the year as a floor plus a capped buffer, "healthcare is unpredictable" becomes "healthcare lands in a range I've already planned for."

On this page

- What is healthcare cost forecasting?

- The Floor-Ceiling Method

- When you need a healthcare forecast

- How to forecast your healthcare costs: a 5-step framework

- A worked example: the Rivera family

- Example healthcare budgets by situation

- Frequently asked questions

- How CostKits does this for you

What is healthcare cost forecasting?

Healthcare cost forecasting is estimating, in advance, what you'll spend on medical care over a defined period — usually a plan year — so you can budget for it instead of reacting to bills as they arrive. A good forecast isn't a single number; it's a planned range with a monthly funding amount attached.

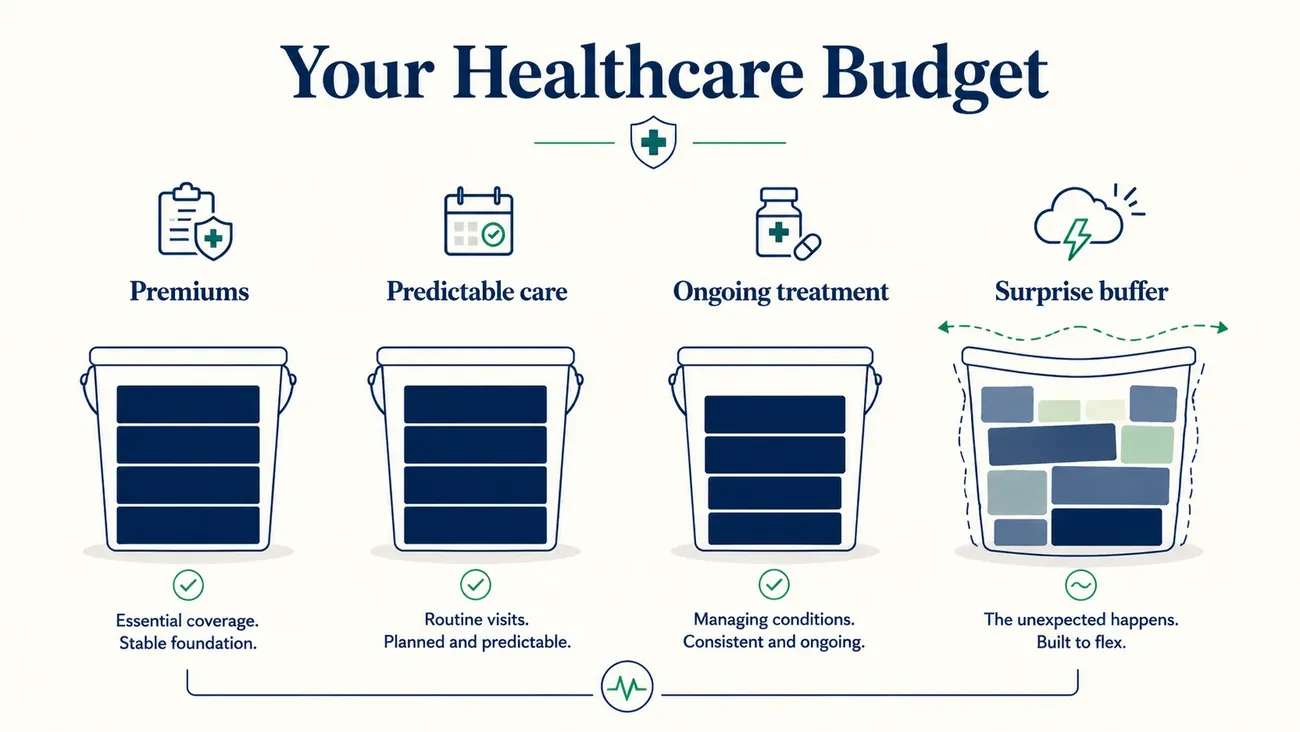

Forecasting works because your spending breaks into four buckets, three of which are predictable:

- Premiums — what you pay every month to have coverage, whether or not you use care. For most families this is the largest and steadiest line.

- Predictable care — routine and preventive visits, dental, vision, the checkups and refills you can see coming.

- Ongoing treatment — prescriptions, therapy, or a chronic condition you already manage. Medium predictability.

- Surprise buffer — the injury, new diagnosis, or procedure you didn't expect. This is the only genuinely unpredictable bucket — and it's the one your plan caps.

The two numbers that anchor the whole forecast are your deductible (what you pay before your plan starts sharing covered costs) and your out-of-pocket maximum (the ceiling on what you can owe for covered, in-network care in a plan year). Once you hit the out-of-pocket maximum, the plan pays 100% for the rest of the year. That ceiling is what makes the unpredictable bucket plannable: your worst case isn't infinite — it's a number printed on your plan's Summary of Benefits and Coverage.

The Floor-Ceiling Method

The simplest way to think about healthcare cost forecasting is as a range between two anchors:

| What it means | Where you find it | |

|---|---|---|

| Floor | Last year's actual out-of-pocket spending | Your EOBs and bills from last year |

| Ceiling | Your plan's out-of-pocket maximum | Your Summary of Benefits and Coverage |

| Forecast | Somewhere between the two, adjusted for known events | The 5-step framework below |

Floor = what a normal year costs you. Ceiling = your worst case, fully defined by your plan. Everything between them is plannable.

Healthcare budgeting becomes easier when you treat the out-of-pocket maximum as the ceiling and last year's spending as the floor — then build your forecast somewhere in between, adjusted for what you already know is coming.

One important nuance on the floor: if last year was unusually expensive — the birth of a child, a major surgery, an unexpected hospitalization — it's not a reliable baseline for next year. Use your best estimate of a "normal" year instead, or use the average of the two most recent years. When in doubt, build in a little extra cushion. It's better to end the year with a small amount of unspent savings than to come up short mid-year.

When you need a healthcare forecast

A forecast is most valuable at specific moments, not as a constant worry. Build or revisit one when:

- You're choosing a plan at open enrollment. Comparing a lower-premium/higher-deductible plan against a higher-premium/lower-deductible one is impossible without forecasting how much care you expect to use.

- The plan year is starting. Premiums, deductibles, and out-of-pocket maximums often reset or change in January (or whenever your plan year begins) — the right moment to set a 12-month plan.

- You know a big event is coming. A planned surgery, a pregnancy, orthodontia, or a new specialty prescription all move the number enough to plan around deliberately.

- Your situation just changed. A new diagnosis, a new job and plan, a new dependent, or a child aging off your coverage each warrant a fresh forecast.

- You're deciding when to schedule elective care. Because deductibles reset each plan year, the timing of a procedure can change what you pay — forecasting tells you whether to pull care into this year or defer it.

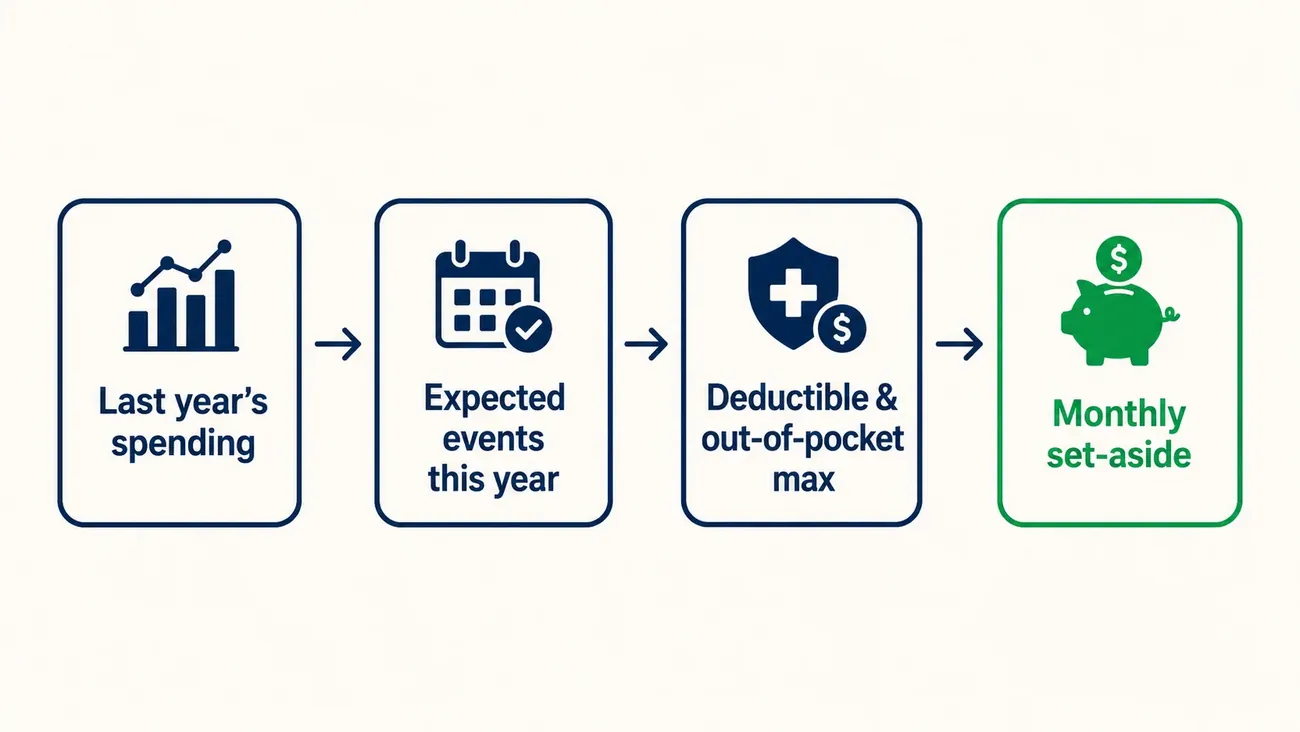

How to forecast your healthcare costs: a 5-step framework

This is the core framework. Work through it once and you'll have both an annual budget and a monthly set-aside. Each step feeds the next.

Step 1 — Add up last year's spending

Pull last year's medical bills and Explanations of Benefits (EOBs) and total what you actually paid out of pocket — not what was billed, but what came out of your pocket after insurance. Include premiums, copays, coinsurance, prescriptions, dental, and vision. This is your baseline: roughly what a "normal" year costs you with no major surprises. If you can't reconstruct it precisely, a reasonable estimate is fine; you're setting a starting point, not filing taxes.

Note on unusual years: if last year included a birth, a major surgery, or a hospitalization, it may overstate your typical annual spending. Use the lower of the past two years, or estimate a normal year from scratch, and build in a little conservatism — leftover savings at year-end is a much better outcome than a shortfall mid-year.

Step 2 — List the major events you expect this year

Write down any care you already know is coming, with a rough cost and rough timing for each: a planned procedure, a pregnancy and delivery, ongoing physical therapy, a new prescription, major dental work. Don't have an exact price? Use a range — our procedure cost guides can anchor an estimate for common procedures like a colonoscopy, an MRI, or childbirth. The goal is to stop being surprised by the category, not to nail the cent.

Step 3 — Look up your deductible and out-of-pocket maximum

Find these two numbers on your plan's Summary of Benefits and Coverage. Note both the individual and family figures if you're on a family plan, and note your plan-year start date — the day the accumulators reset to zero. These define the floor and the ceiling of what the year can cost you. (If you're fuzzy on how they interact, our guide to the deductible vs. out-of-pocket maximum breaks it down.)

Step 4 — Size your surprise buffer against the out-of-pocket max

Here's the part most budgets miss. Your worst case for the year is capped: it's the gap between what you've already spent and your out-of-pocket maximum. So your buffer doesn't need to be limitless — it needs to be a sensible fraction of that gap. Set it larger if a big event is likely or you manage a chronic condition; set it smaller in a quiet year. Sizing the buffer against the ceiling rather than against fear is what turns anxiety into a number.

Step 5 — Total it and divide by twelve

Add your premiums, predictable care, ongoing treatment, expected events, and buffer into a single annual healthcare budget. Then divide by 12. That monthly figure is the amount to set aside — ideally as an automatic transfer into a dedicated account, or a health savings account (HSA) if your plan is HSA-eligible. The money is now decided on in advance, not borrowed from a future month when the bill lands.

A worked example: the Rivera family

Illustrative example — the numbers below are made up to show the method, not real prices or averages. Use your own plan's figures.

The Riveras are a family of four. Last year, with no major events, they paid about $6,000 out of pocket — mostly premiums, plus routine visits and prescriptions. This year, they know one thing is coming: a knee procedure for one parent, which their forecast pegs at roughly $4,000 out of pocket given where it falls against their deductible.

Their plan has a $4,000 family deductible and a $12,000 family out-of-pocket maximum. Walking the framework:

- Baseline (last year): $6,000

- Known event (knee procedure): + $4,000

- Surprise buffer: because they'll likely approach their out-of-pocket max this year anyway, they set a modest $1,000 buffer rather than a large one — the ceiling already limits the downside.

- Annual budget: about $11,000

- Monthly set-aside: $11,000 ÷ 12 ≈ $917

Notice what the out-of-pocket maximum did: it told the Riveras their absolute worst case was $12,000 plus premiums — not some unknowable figure. That ceiling is why they could set a small buffer with confidence instead of guessing high out of fear. In a year with no planned procedure, the same family might budget closer to their $6,000 baseline plus a slightly larger buffer, landing near $640 a month. Same framework, different inputs.

Example healthcare budgets by situation

The following examples show how the Floor-Ceiling Method applies across common household situations. All figures are illustrative — use your own plan numbers and spending history for your actual forecast.

Single adult, healthy year

Profile: 28-year-old, employer HDHP, minimal care expected

| Budget line | Amount |

|---|---|

| Floor (last year's spending) | $1,800 |

| Known events | $0 |

| Surprise buffer (25% of OOP gap) | $600 |

| Annual budget | $2,400 |

| Monthly set-aside | $200 |

The OOP max provides the ceiling ($4,000); the buffer is sized small for a healthy, low-use year. An HSA contribution is ideal here — unused funds roll over.

Couple, routine care

Profile: Two adults in their late 30s, PPO plan, annual checkups and one specialist

| Budget line | Amount |

|---|---|

| Floor (last year's spending) | $4,200 |

| Known events | $800 (specialist + labs) |

| Surprise buffer | $1,000 |

| Annual budget | $6,000 |

| Monthly set-aside | $500 |

A couple with predictable, low-complexity care fits cleanly between floor and ceiling. The buffer is modest because the care pattern is consistent.

Family of four, typical year

Profile: Two adults, two kids, PPO plan, pediatric care + adult checkups

| Budget line | Amount |

|---|---|

| Floor (last year's spending) | $6,500 |

| Known events | $1,200 (braces consult, PT for one parent) |

| Surprise buffer | $1,800 |

| Annual budget | $9,500 |

| Monthly set-aside | $792 |

Kids add frequency but not severity — most pediatric care is routine. The buffer covers a moderate illness or urgent care visit.

High-deductible plan user with HSA

Profile: Single adult, $4,000 deductible HDHP, generally healthy

| Budget line | Amount |

|---|---|

| Floor (last year's spending) | $2,200 |

| Known events | $0 |

| Surprise buffer | $1,800 (sized toward deductible) |

| Annual budget | $4,000 |

| Monthly set-aside | $333 (fund via HSA) |

The buffer is sized near the deductible because that's the out-of-pocket exposure before the plan shares costs. The monthly set-aside goes into an HSA — triple tax advantage applies.

Chronic condition family

Profile: Family of four, one member on specialty medication + regular specialist visits

| Budget line | Amount |

|---|---|

| Floor (last year's spending) | $9,000 |

| Known events | $3,000 (ongoing medication, quarterly specialist) |

| Surprise buffer | $1,500 (OOP max approaches; gap is small) |

| Annual budget | $13,500 |

| Monthly set-aside | $1,125 |

When one member has a chronic condition, the floor is naturally higher and the gap to the OOP max narrows. The buffer is smaller because the plan's ceiling is already close — and because tracking deductible accumulation matters more in these households.

Related Cost Information

The pattern across every example is the same: floor (last year) + known events + buffer (sized against the OOP max ceiling) = annual budget ÷ 12 = monthly set-aside. The inputs change; the method doesn't.

Frequently asked questions

How much should I budget for healthcare each year?

Start from what you actually paid last year, then add the cost of any major events you already know are coming and a buffer for surprises. Your worst case is capped by your plan's out-of-pocket maximum, so your annual budget should land between last year's routine spending and that ceiling — closer to the ceiling in a year with a planned procedure, closer to routine in a quiet year.

How do I forecast my healthcare costs for the year?

Add up last year's out-of-pocket spending as a baseline, list the major events you expect this year with rough costs, look up your deductible and out-of-pocket maximum, size a surprise buffer against that maximum, then total everything and divide by 12 for a monthly set-aside amount.

What is the Floor-Ceiling Method for healthcare budgeting?

The Floor-Ceiling Method is a framework for forecasting healthcare costs by anchoring to two known numbers: your floor (last year's actual out-of-pocket spending) and your ceiling (your plan's out-of-pocket maximum). Your forecast falls somewhere between these two, adjusted for any major events you already know are coming. The ceiling is what makes the unpredictable part plannable — your worst case isn't a guess, it's a number printed on your plan documents.

What if last year was unusually expensive?

If last year included a major event — a birth, a surgery, a hospitalization — it's not a reliable floor for next year. Use your best estimate of a typical year, or average the past two years. When in doubt, build in a little extra cushion: ending the year with leftover savings is a better outcome than running short mid-year.

What's the difference between a deductible and an out-of-pocket maximum?

Your deductible is what you pay yourself before your plan starts sharing covered costs. Your out-of-pocket maximum is the most you can owe for covered, in-network care in a plan year — once you reach it, the plan pays 100% for the rest of the year.

How do I predict medical expenses when I don't know what will happen?

You don't predict the specific event — you size the range. Premiums and routine care are predictable and form the floor. The unpredictable part is capped by your out-of-pocket maximum, so you set a buffer between the two rather than trying to guess the exact bill.

When is the best time to make a healthcare budget?

At open enrollment or the start of your plan year, when you choose your coverage and your premiums, deductible, and out-of-pocket maximum may change. That's when you have the numbers you need to set a 12-month plan.

Should I include premiums in my healthcare budget?

Yes. Premiums are what you pay every month to have coverage, whether or not you use care, and for most families they're the largest and most predictable line in the budget. Include them even if they're deducted from your paycheck.

How much should my surprise buffer be?

A reasonable starting point is a fraction of the gap between what you expect to spend and your out-of-pocket maximum — larger if you have a procedure on the horizon or a chronic condition, smaller in a quiet year. The maximum is the ceiling, so the buffer never needs to exceed it.

Can an HSA help me budget for healthcare?

If your plan is HSA-eligible, a health savings account is a tax-advantaged place to hold your monthly set-aside. Contributions are pre-tax, growth is tax-free, and withdrawals for qualified medical expenses are tax-free. Unused funds roll over year to year — making an HSA especially powerful for healthy years when you underspend your forecast. Contribution limits are set each year by the IRS.

Does the time of year I get a procedure change what I pay?

It can. Deductibles and out-of-pocket maximums reset every plan year. An elective procedure scheduled before your plan year resets may fall in the same year as other care you've already paid toward, while the same procedure after the reset starts a fresh deductible. If you're near your deductible late in the year, pulling planned care into that year may save money.

What if my actual spending doesn't match my forecast?

That's expected — a forecast is a plan, not a prediction. Track your real spending against it as bills arrive, and adjust the monthly set-aside if a major event changes the picture. Most years will come in under your buffer; the point is that the high-cost year doesn't catch you unprepared.

How do I budget for healthcare at open enrollment?

Run the 5-step framework against each plan you're considering. The plan with the lower premium often has a higher deductible and out-of-pocket max — which raises your ceiling and may require a larger buffer. The right choice depends on how much care you expect to use; a healthy year favors a lower-premium plan, while a high-use year often favors a plan with a lower out-of-pocket max.

What counts as an out-of-pocket expense for budgeting purposes?

Everything you pay directly: premiums, deductibles, copays, coinsurance, and any cost-sharing for covered services. Dental, vision, and prescriptions may fall outside your medical plan's accumulator — check your plan documents. Out-of-network care often has a separate, higher out-of-pocket maximum.

How is a family deductible different from an individual deductible?

Family plans typically have both an individual deductible (which each member hits separately) and a family deductible (a combined threshold for the household). Once a family member hits their individual deductible, the plan starts sharing costs for them — even if the family aggregate hasn't been reached. Both limits matter for forecasting.

How CostKits does this for you

Doing this once on paper is the best way to understand it. Keeping it current as premiums change and bills arrive is the part worth automating — and that's exactly what the CostKits tools do:

- Forecast turns your plan and known events into a projected annual cost and a monthly set-aside, then keeps the running total as the year unfolds.

- Analyze checks a bill or EOB against your estimate and your plan, so an overcharge doesn't quietly blow your forecast.

- Track watches your deductible and out-of-pocket maximum fill in automatically, so you always know where you stand against the ceiling that anchors your buffer.

Forecast once, fund it monthly, and let the tracking run — that's how a year of healthcare goes from a source of dread to a line in your budget like any other.

Forecasting your healthcare costs is easier with a worksheet in hand.

The free Annual Healthcare Budget Planner gives you:

- ✓ A one-page annual budget worksheet that produces your monthly set-aside

- ✓ A major-event checklist so a surgery or new baby never blindsides your plan

- ✓ A deductible worksheet that anchors your buffer to your out-of-pocket max

- ✓ Worked forecast examples you can model your own year on

- ✓ Print-and-fill — bring it to open enrollment or the start of your plan year

Free — we'll email it to you now.

We'll email it to you immediately. No account required, no spam.

Related Articles

Interested in understanding healthcare costs and managing your medical expenses?

- Deductible vs Out-of-Pocket MaximumLearn how insurance cost-sharing works and what you actually pay

- Cost ExplorerBrowse procedures and compare prices across the country

- CT Scan Cost GuideFind detailed CT scan pricing for your state

- MRI Cost GuideCompare MRI pricing and understand imaging costs

- X-Ray Cost GuideCompare X-ray pricing across states—one of the most affordable imaging procedures

- Colonoscopy Cost GuideUnderstand colonoscopy pricing and your out-of-pocket costs by insurance type

- New GuidesExplore our latest healthcare guides on costs, insurance, and medical billing

About the Author

John Caruso, FSA, MAAA

Healthcare actuary with 20+ years of experience in insurance pricing, medical billing systems, and healthcare cost analytics.

Connect on LinkedIn →Ready to take control of your healthcare costs?