Learn how to estimate your annual healthcare spending using deductibles, coinsurance, and the Healthcare Cost Forecast Calculator.

How to Estimate Your Healthcare Costs This Year (Free Calculator)

Staring at a medical bill and wondering how much more is coming? You're not alone. Americans spend an average of $4,500 per person annually on healthcare. But that number is almost meaningless when you're trying to predict your actual costs for your family this year.

The brutal truth is that healthcare spending is almost impossible to predict with precision. But it's not impossible to estimate with reasonable confidence. The difference between guessing and forecasting can mean the difference between financial stress and genuine peace of mind.

In this guide:

- Why healthcare costs are unpredictable

- The four numbers that determine your spending

- Average healthcare costs in the U.S.

- How to estimate your costs

- Healthcare cost forecast calculator

Healthcare Cost Calculator: How to Estimate Your Medical Spending

Instead of struggling with complex spreadsheets, use the CostKits Healthcare Cost Forecast Calculator to get your personalized estimate. Enter your insurance plan details, your age, and your expected medical services. The calculator does the math for you, showing you best-case, expected, and worst-case scenarios.

Use the Healthcare Cost Forecast Calculator – it's free and takes less than 5 minutes.

Why Healthcare Costs Are So Hard to Predict

Your healthcare spending depends on three things you can't fully control: whether you get sick, when you get sick, and where you seek treatment.

Unpredictable medical events. A minor injury that requires an ER visit. A chronic condition that flares up. A preventive screening that uncovers something else. You can plan a budget based on historical spending or insurance estimates, but life happens. Medical emergencies, by definition, are emergencies.

Insurance cost-sharing mechanisms. Your insurance plan splits costs between you and your insurer using deductibles, coinsurance percentages, and out-of-pocket maximums. This means the amount you owe isn't a simple percentage of the bill. It depends on how much you've already spent that year, which insurance tier the provider falls into, and whether the service is covered. A $3,000 MRI can cost you $0 if you haven't met your deductible (you owe the full $3,000 out of pocket until you do) or $300 if you've already spent enough to meet your deductible and you're in the coinsurance phase.

Price variation across providers. Even within the same insurance network, the same procedure can cost dramatically different amounts at different facilities. A study by the RAND Corporation found that the cost of a CT scan varies by over 1,000% depending on where you get it. That's not a typo.

These three factors combine to create uncertainty that feels paralyzing. But here's the good news: while you can't predict individual medical events with certainty, you can make an educated forecast based on your insurance plan design, your age, and your historical medical utilization. That forecast won't be perfect, but it will be actionable.

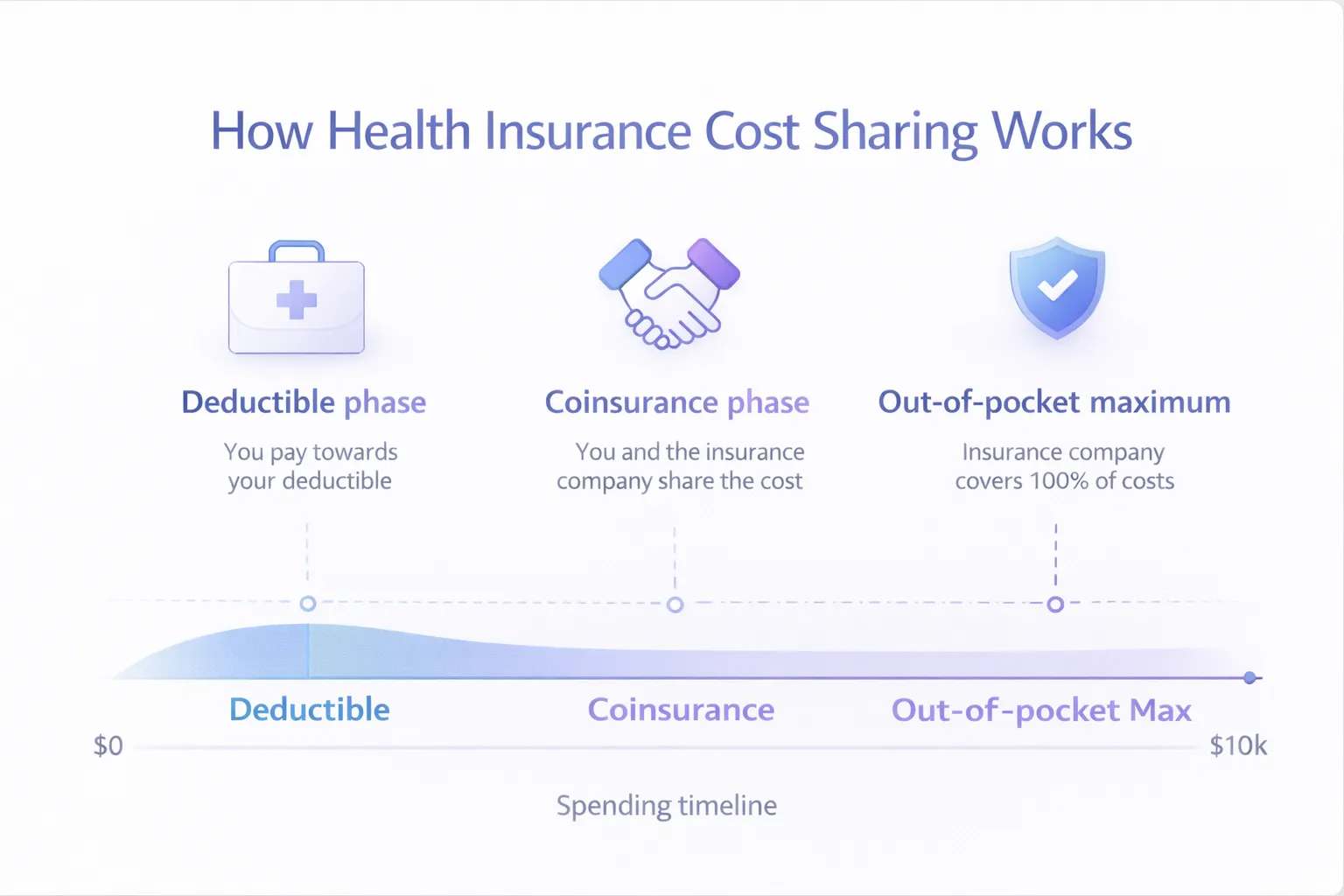

The Four Numbers That Determine Your Healthcare Costs

Before we dive into estimation strategies, let's define the four financial levers that control how much you'll actually pay for healthcare this year:

Deductible

Your deductible is the amount of money you must pay out of your own pocket for healthcare services before your insurance plan starts helping to pay. If your deductible is $1,500, you pay 100% of eligible medical bills until you've paid $1,500. After that, your insurance begins to share the cost with you.

Key point: Many people assume that once they're insured, they won't have significant costs. In reality, if you hit a medical event early in the year, you may pay your entire deductible out of pocket immediately.

Coinsurance

After you've met your deductible, your insurance company doesn't pay 100% of your bills. Instead, you and your insurer share costs using a percentage split. This is called coinsurance. A common arrangement is 80/20, meaning your insurance pays 80% of covered costs and you pay 20%. Some plans use 70/30 or 75/25.

Key point: Coinsurance continues to apply until you hit your out-of-pocket maximum. That's the next number.

Out-of-Pocket Maximum

This is your financial safety net. Your out-of-pocket maximum is the highest amount you'll pay for covered healthcare services in a given year. Once you reach this number, your insurance pays 100% of covered costs for the rest of the year.

For 2026, the IRS sets limits: $9,450 for individual coverage and $18,900 for family coverage. Your actual plan's out-of-pocket maximum may be lower.

Key point: This is your worst-case scenario number. No matter what happens medically, you will not pay more than this amount out of pocket (for covered services).

Medical Utilization

This is the medical care you'll actually use. It includes preventive care (which is usually covered at 100% under the Affordable Care Act), primary care visits, specialist visits, lab work, imaging, procedures, medications, and any hospitalizations.

Your utilization depends on your health status, age, chronic conditions, and whether you're due for preventive screenings. A 25-year-old in perfect health likely has low utilization. A 65-year-old managing multiple chronic conditions has much higher utilization.

Key point: This is the most variable and unpredictable number, but it's also the most important for forecasting.

Average Healthcare Spending in the U.S.

To anchor your thinking, here's what Americans actually spend on healthcare according to the Medical Expenditure Panel Survey (MEPS) and CMS National Health Expenditure data:

By individual:

- Average per person: $4,500–$5,200 annually (includes all ages and health statuses)

- Median per person: $1,200–$1,500 (half of people spend less, half spend more)

- Age 18–34: $1,800–$2,400 per person

- Age 35–54: $3,500–$4,200 per person

- Age 55–64: $6,200–$7,800 per person

- Age 65+: $10,500–$13,000+ per person (note: Medicare covers much of this)

By household:

- Family of 4 (2 adults, 2 children): $8,000–$12,000 annually

- Household with one chronic condition: $6,000–$15,000 annually

- Household with multiple chronic conditions: $15,000–$40,000+ annually

Important caveat: These are national averages. Your actual costs depend on your insurance plan design, your location, your healthcare provider choices, and your specific medical needs.

Data sources: These figures are based on the Agency for Healthcare Research and Quality (AHRQ) Medical Expenditure Panel Survey (MEPS) and CMS National Health Expenditure Accounts, which track actual healthcare spending across the U.S. population.

How to Estimate Your Healthcare Spending for the Year

Here's the step-by-step approach:

Step 1: Know your insurance plan numbers. Write down: deductible, coinsurance percentage, out-of-pocket maximum, and whether specific services (preventive, mental health, prescriptions) have different cost-sharing.

Step 2: Estimate your utilization. Think about your expected medical care: annual preventive visits, chronic condition management, prescription medications, planned procedures, anticipated specialist visits. Be realistic, not optimistic.

Step 3: Calculate deductible spending. Your first X dollars of bills will go toward your deductible. In most plans, preventive care doesn't count toward the deductible (covered at 100%), but other services do.

Step 4: Calculate coinsurance spending. Once you've met your deductible, you'll pay your coinsurance percentage until you hit your out-of-pocket maximum. Multiply your expected medical bills (after deductible) by your coinsurance percentage.

Step 5: Cap at your out-of-pocket maximum. If your projected costs exceed your out-of-pocket maximum, your actual out-of-pocket cost is the out-of-pocket maximum, not the higher number.

Step 6: Add premiums and out-of-network costs. Don't forget that your monthly insurance premiums are part of your total annual healthcare cost. Also budget for any expected out-of-network services.

This is where the math gets tedious and error-prone, especially for families with multiple members on different cost-sharing tiers or with expected medical events.

Use the Healthcare Cost Forecast Calculator

The CostKits Healthcare Cost Forecast Calculator automates this entire process. Instead of doing this math yourself, enter your insurance plan details, your age, and your expected medical services. The calculator does the forecasting for you using actuarial data.

The calculator uses actuarial data on medical utilization by age and health status, combined with your specific insurance plan design, to project your most likely annual healthcare spending and show you the range of possibilities from best case to worst case.

Use the Healthcare Cost Forecast Calculator – it's free and takes less than 5 minutes.

The forecast gives you three scenarios:

- Best case: Minimal medical utilization, you meet your deductible but little coinsurance (typical year with just preventive care and one or two routine visits)

- Expected case: Your most probable spending based on age and health status (historical data for people like you)

- Worst case: Your out-of-pocket maximum (the scenario where you face a significant medical event)

With this forecast in hand, you can budget realistically, adjust your FSA or HSA contributions, and know what financial stress you should prepare for.

Example Healthcare Cost Forecast

Let's walk through a real example: the Garcia family.

The Scenario:

- Parents: both age 42, both with managed hypertension (controlled with medication)

- Children: ages 8 and 11, both healthy

- Insurance: Family PPO plan with $4,000 family deductible, 80/20 coinsurance, $13,500 out-of-pocket maximum

- Monthly premium: $1,200 (already budgeted separately)

- Expected medical events: routine preventive visits, one specialist visit for hypertension management, routine dental (not covered by medical insurance), prescription medications

Forecast Breakdown:

Preventive care (covered at 100%, doesn't count toward deductible):

- 2 adult annual checkups: $0 out of pocket

- 2 children annual checkups: $0 out of pocket

- 1 mammogram: $0 out of pocket

- Vaccines: $0 out of pocket

- Total preventive: $0 (fully covered)

Chronic condition management (counts toward deductible):

- 2 specialist visits for hypertension: $600 (these go toward the deductible)

- Lab work: $400 (toward deductible)

- Subtotal: $1,000 in medical bills

Prescriptions (typically subject to copay or coinsurance):

- Hypertension medications for both parents: $120/month = $1,440/year

- Allergy medication for one child: $20/month = $240/year

- Subtotal: $1,680/year (some of this goes toward deductible, remainder toward coinsurance)

Calculation:

- Medical bills before deductible: $1,000 (specialist + labs)

- Remaining deductible after medical bills: $3,000

- Prescriptions: $1,680 (let's assume $1,000 applies toward the remaining deductible, leaving $680 subject to coinsurance)

- At 80/20 coinsurance: $680 × 20% = $136

- Total out-of-pocket projection: $1,000 (deductible) + $136 (coinsurance) = $1,136

What if something unexpected happens?

- If one parent requires an ER visit and imaging: add $2,000 in bills

- These would be subject to coinsurance (deductible already met): $2,000 × 20% = $400 additional

- New total: $1,536

- Still well below the $13,500 out-of-pocket maximum

This example shows how forecasting works: the Garcia family can reasonably expect to pay around $1,100-$1,500 in medical costs this year (plus their $14,400 annual premiums), with a worst-case cap of $13,500 from the out-of-pocket maximum.

For more on how insurance plans work, see our guide on how to read your EOB line by line.

How Insurance Caps Your Worst-Case Healthcare Costs

The out-of-pocket maximum is the most important number in your insurance plan because it's your financial safety net. It represents the absolute most you'll have to pay out of your own pocket in a given year for covered healthcare services.

Here's why this matters: if you're hit with a major medical event (a serious accident, an unexpected hospitalization, a cancer diagnosis requiring surgery and chemotherapy), your insurance plan limits your personal financial liability. Once you've paid your out-of-pocket maximum, your insurance covers 100% of all additional covered services for the rest of the year.

This is the insurance company's promise to you, and it's legally enforceable. You're protected.

Important caveat: The out-of-pocket maximum applies only to covered services and in-network providers. If you go out of network without authorization, costs may not count toward your out-of-pocket maximum, and you could face bills beyond that cap.

Plan Your Healthcare Budget for the Year

Once you have your healthcare cost forecast, here's how to build it into your overall financial plan:

1. Adjust your FSA or HSA contributions. If you expect $8,000 in out-of-pocket costs and you're eligible for an FSA or HSA, contribute that amount (up to annual limits). This money is tax-free, effectively reducing your costs by 20–40% depending on your tax bracket.

2. Build a healthcare emergency fund. Even with good forecasts, medical emergencies are unpredictable. If your out-of-pocket maximum is $8,000, ideally you'd have that amount available in a dedicated savings account or emergency fund.

3. Review your plan every year. Healthcare plans change. Your insurance provider may adjust deductibles, coinsurance, or out-of-pocket maximums. Your employer may offer a different plan. Review annually during open enrollment and recalculate your forecast if your plan changes.

4. Track your spending throughout the year. Keep a running tally of what you've paid toward your deductible and out-of-pocket maximum. This helps you understand where you stand and adjust your expectations. Most insurance companies provide online dashboards showing your progress toward both numbers.

5. Don't overpay for medical bills. Once you know your forecast, you know what you can reasonably afford. When you receive a medical bill, verify it's correct (check our guide on fighting medical bill errors if something looks off), and don't hesitate to negotiate if you're facing surprise charges.

For strategies on managing unexpected bills, also check out our article on how to negotiate medical bills.

Related Reading

- What Does a CT Scan Really Cost: The Shocking Price Differences Explained – Understand why medical prices vary so dramatically

- Deductible vs. Out-of-Pocket Max: What Families Need to Know – Deep dive into the two key plan numbers

- EOB vs. Medical Bill: Complete Guide – Understanding your documents

- How to Write a Claim Appeal Letter and Save Money – Fight back against denials

- How to Read Your Medical Bill: A Step-by-Step Guide for Families – Master the fundamentals

About the Author

John Caruso, FSA, MAAA is a healthcare actuary with 20+ years of experience in insurance pricing, medical billing systems, and healthcare cost analytics. He founded CostKits to help families understand and control their healthcare expenses. Connect on LinkedIn →

John holds the Fellow of the Society of Actuaries (FSA) and Member of the American Academy of Actuaries (MAAA) designations. His work has focused on analyzing billions of medical claims to identify pricing patterns, billing errors, and cost-reduction opportunities across commercial and Medicare populations.

The Bottom Line

Healthcare costs are unpredictable, but they're not unknowable. By understanding your insurance plan, estimating your medical utilization, and calculating your financial exposure, you can create a realistic budget and prepare for both expected and unexpected healthcare expenses.

The easiest way to do this? Use the CostKits Healthcare Cost Forecast Calculator. Enter your information, get your forecast, and move forward with confidence.

Your healthcare costs shouldn't be a source of financial stress. They should be a number you understand, can plan for, and can manage. Start by getting your forecast today.